Chapter 13 Bankruptcy in Maricopa County

Scottsdale Chapter 13 Bankruptcy Lawyers

If you are considering filing for chapter 13 bankruptcy in Scottsdale, Arizona, our Scottsdale bankruptcy lawyers may be of great assistance. Do you have a regular income but are experiencing severe debt problems? If so, chapter 13 bankruptcy might be the debt relief solution that you seek. Seek out the guidance of a chapter 13 bankruptcy attorney to find out if your particular situation may be right for debt relief protection of filing chapter 13 bankruptcy in Scottsdale, Arizona.

Bankruptcy filing rates in Scottsdale and throughout Maricopa County are on the rise. The 2 most common types of bankruptcy filed under federal law are chapter 7 and chapter 13 bankruptcy. If you are eligible for a Chapter 13, your unsecured debts, (such as credit card debt), are combined. A chapter 13 payment plan is created based on your disposable income. You don’t have to worry about this plan as you will still have enough money left over to make payments on secured debt, such as house and vehicle payments. Chapter 13 permits you to adjust your debts, retain your assets and pay off the money you owe, normally over a 3 to 5 year period.

There are several differences between Chapter 7 and Chapter 13 bankruptcy. If you are considering bankruptcy as a means to get out of debt, consult with an experienced Arizona bankruptcy law attorney. We can help you determine the chapter and best debt-relief action to take for your specific debt and case.

CHAPTER 13 bankruptcy FAQs

FAQs for Our Scottsdale Bankruptcy Lawyers

ANSWER:

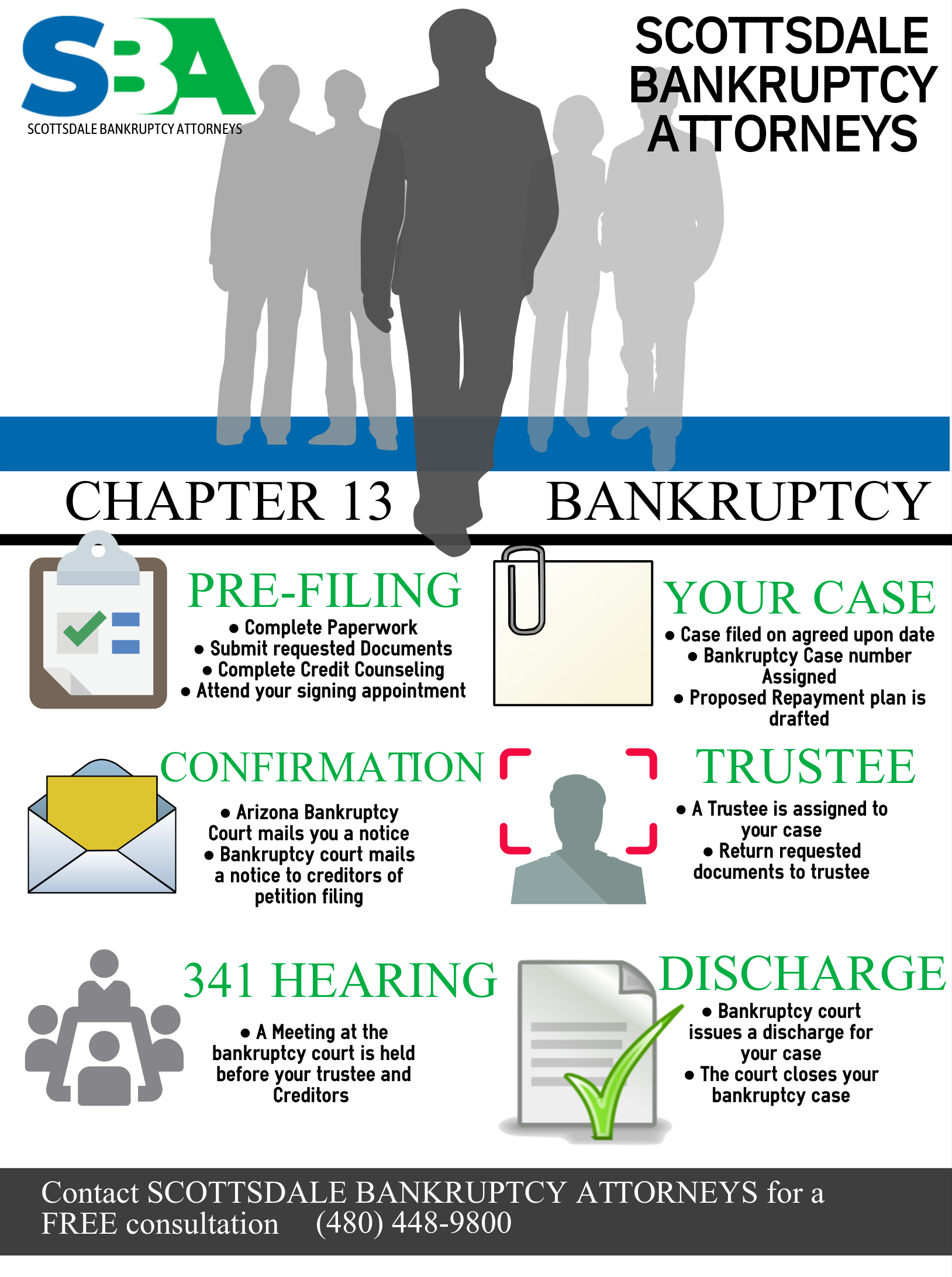

Chapter 13 Bankruptcy is devised for people who are employed but still struggle with debt, which is why it is also called a wage earner’s bankruptcy. A payment plan will be calculated based on the filer’s income and types of debts they have. High priority debts must be paid in full in the plan, while low priority debts may be discharged after only partial repayment. The person declaring bankruptcy must submit a petition that details their financial situation, along with a mailing matrix of all of their creditors and a proposed schedule for their payment plan.

The filer will need to take one credit counseling course before the petition is filed. Once the petition is filed, a trustee will be assigned to oversee the case. The filer will later receive a court date for their 341 Meeting of Creditors. After the filer has attended this mandatory hearing, they will take a second credit counseling course and continue with their payment plan. There is also a hearing to confirm the schedule of the payment plan. The payment plan will last 3-5 years, depending on the filer’s income level. Debts will be discharged once the payment plan is completed.

ANSWER:

Chapter 13 is more complicated than Chapter 7 bankruptcy, and most people who file choose to do so with attorney representation. You can file without an attorney, but that is rarely a good idea. The success rate for Chapter 13 bankruptcies filed without an attorney is less than 1 percent.

ANSWER:

A trustee will be assigned to review your petition and collect your plan payments to distribute among your creditors. Your trustee will likely request additional documents after your case has been filed to confirm that everything in your petition is true and correct. The trustee will also be present at your 341 Meeting of Creditors, where they may have additional questions or requests for documentation. The trustee will be present at your plan confirmation, and review all of your creditors’ claims.

ANSWER:

A joint bankruptcy petition may be filed with a spouse. You can’t file a joint bankruptcy with a child, parent, or any other you aren’t legally married to. If you are married, it is usually simpler to include your spouse in your filing as opposed to filing a single petition. Your payments will be calculated using both of your incomes, so you may not have sufficient income to make your plan payments if you and your spouse were to divorce. Even if you can afford your plan payments after a divorce, the property division section of divorce will be delayed, possibly until your bankruptcy is completed. If you are married and still think you want to file a single Chapter 13 petition, you should consult an attorney to make sure it is feasible for you.

ANSWER:

The filing fee for a Chapter 13 bankruptcy is $310. You will also need to pay fees for both of your credit counseling courses, which could range from $15 to $50 each. Attorney’s fees will be considerably higher. However, your attorney may be willing to take a relatively small down payment and work the rest of their fees into your payment plan.

ANSWER:

The order and amount in which debts are paid will depend on the type of debt and its priority. The first debts to be paid are attorney’s fees and fees paid to the trustee. Once those are paid, secured debts are next, followed by priority debts, and lastly unsecured debts.

Secured debts have some type of collateral attached to them, such as your car or home. Your car loan must be paid in full in your Chapter 13, but you only have to catch up any past due balance and remain current on your mortgage. Your mortgage may or may not be included in your plan, depending on the jurisdiction in which your petition is filed.

Priority debts include child support, spousal support, and certain tax debts. These debts must be paid in full through your Chapter 13 plan, or your plan won’t be approved. Once these debts are paid, the trustee will begin sending payments to your unsecured creditors. Most unsecured creditors will be discharged after your bankruptcy, even if you only pay a small portion of their debts.

ANSWER:

At the end of your payment plan, you may have caught up on past-due payments that will continue after the bankruptcy, and the balances of some unsecured debts may be discharged. When debts are discharged, you are no longer legally obligated to pay them.

ANSWER:

Student loans are unsecured, non-priority debts, meaning they are paid last in the bankruptcy. However, unlike other unsecured non-priority debts like credit cards and medical bills, they will not be discharged at the end of the payment plan. Student loans can only be discharged in rare circumstances through Chapter 7 bankruptcy.

ANSWER:

Conduit payments are included in a Chapter 13 payment plan when the filer is behind on their mortgage payments. The conduit payment will include the filer’s normal monthly payment along with a portion of the past-due balance. The trustee will excuse filers from making conduit payments only in rare circumstances.

ANSWER:

As mentioned above, you will make conduit mortgage payments in your payment plan if you have a balance that needs to be caught up. Catching up will be more affordable when your past-due balance is spread out over the course of 3-5 years. You will also be protected by bankruptcy’s Automatic Stay as long as your case is active. Your home lender will be prevented from foreclosing on your home until your case is discharged or dismissed. If your case is successfully discharged, you will have caught up on your mortgage payments and your lender can only foreclose if you fall behind again.

ANSWER:

The Automatic Stay will also prevent your student lender from pursuing you for payments during the lifespan of your bankruptcy. If your wages are being garnished for your student loan, this will stop during your Chapter 13 payment plan. Your student lender will begin receiving payments along with the other unsecured non-priority creditors, so your balance may still decrease during your Chapter 13. You may still accrue interest on your student loans during your bankruptcy.

Chapter 13 Bankruptcy Attorney Serving Scottsdale and Phoenix

Scottsdale Chapter 13 Bankruptcy Lawyer

Our Scottsdale bankruptcy law firm helps clients in Scottsdale, Phoenix, and throughout Arizona make informed decisions about their financial future. Our Scottsdale bankruptcy attorneys will go over all of the details of your debts to help you figure out whether filing for chapter 13 bankruptcy is the best option or if there are alternatives to filing bankruptcy that may be more appropriate. Our Scottsdale debt relief experts can immediately help stop creditor harassment and constant phone calls, which is generally well known when people are behind on their bill payments.

We will discuss your options during initial consultation and provide you with simple information that explains the bankruptcy process. If it is decided that Chapter 13 is the best route, our approach is very streamlined. There are no lengthy forms to fill out and you will know exactly what to expect in the coming weeks, months and possibly, years. Our Scottsdale chapter 13 bankruptcy lawyers are very experienced in handling chapter 13 bankruptcy filings. We get our plans confirmed quickly and guide you through the whole process of filing chapter 13 bankruptcy and financial freedom.

Contact one of our Scottsdale chapter 13 bankruptcy attorneys from our Scottsdale bankruptcy law firm now to set up a free consultation to go over your options. Call (480) 833-8000 for a free consultation and debt evaluation.

Bankruptcy Attorney Firm 5.0 Star Rated on Avvo

")

Low Fee

Guarantee

File With

$0 Down

Free Case

Consultations

4 Convenient

Locations

Payment Plans

Available